Modelling private wealth accumulation and spend-down in the Italian microsimulation model CAPP_DYN: A life-cycle approach

- Sapienza University of Rome, Italy

- Bank of Italy, Italy

- University of Bologna and CAPP, Italy

- ISER and CAPP, England

- Article

- Figures and data

- Jump to

Figures

{kind=link}

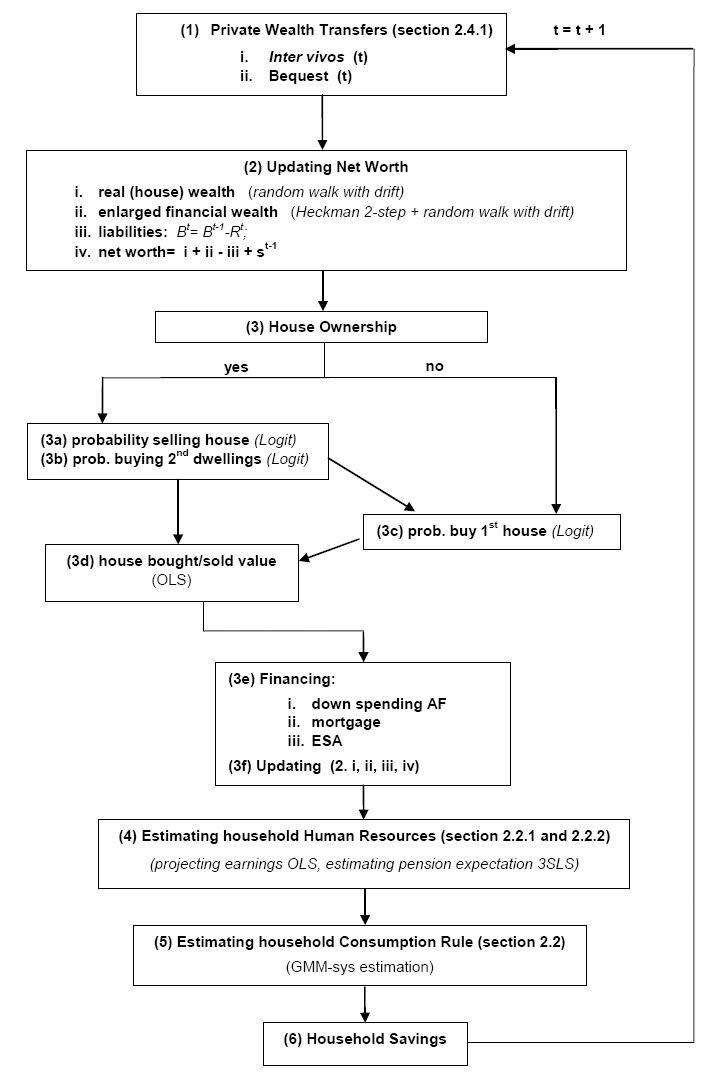

A stylized scheme of formation and transmission of wealth in the wealth module.

{kind=link}

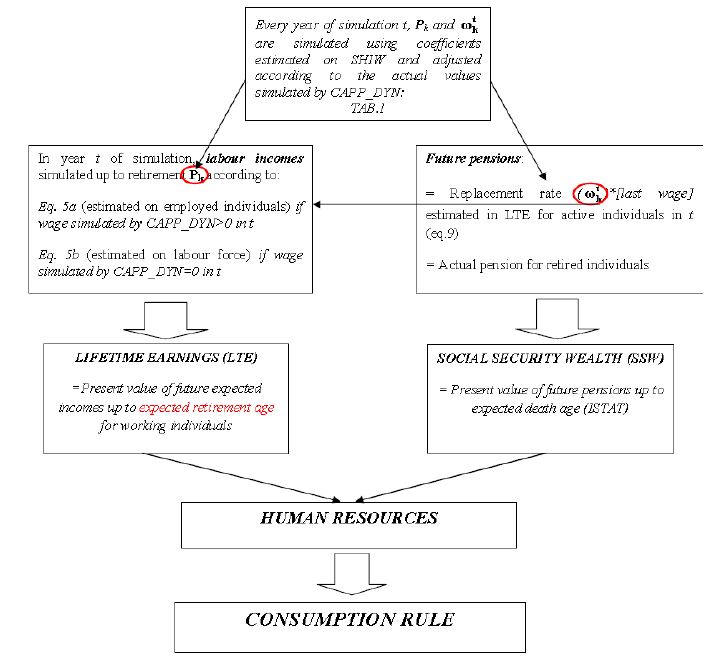

Estimation and simulation of human resources.

{kind=link}

Average equivalent consumption (left) and propensity to save (right) household-head-age-profile.

{kind=link}

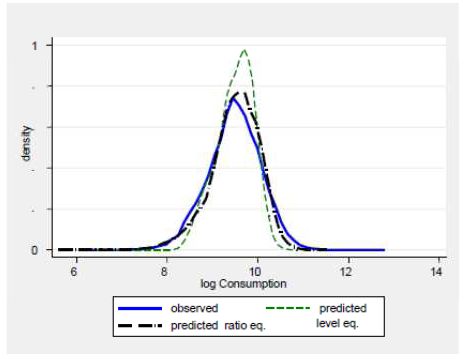

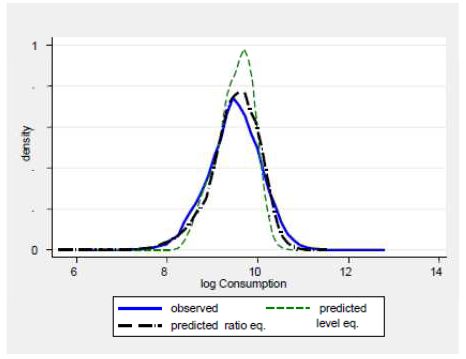

Post-estimation predicted consumption from dynamic model in level vs ratio.

{kind=link}

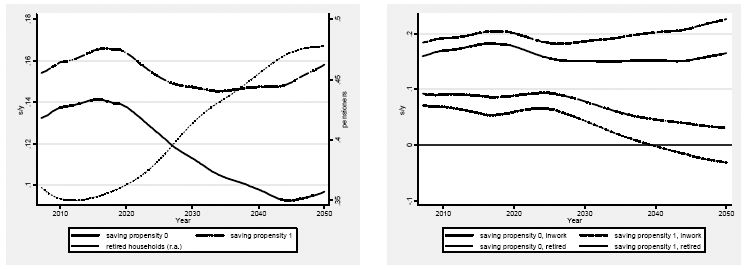

Average saving propensity (left), propensity to save for active households vs. for retired households (right), 2008–2050.

{kind=link}

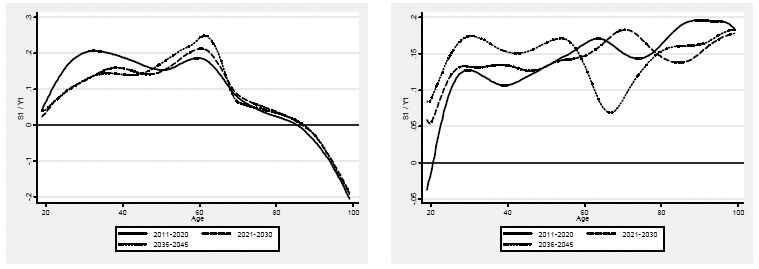

Propensity to save by age, LC (left) vs. NS (right) simulation, 2011–2020, 2021–2030, 2036–2045 (averages).

Source: Authors’ computations on simulation results.

{kind=link}

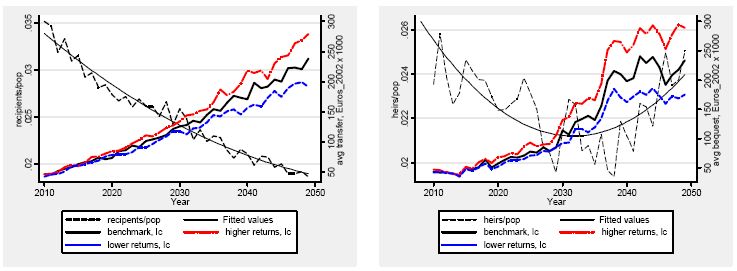

Evolution of iv and mc transfers recipient households’ share and of the average amount received, 2010–2050.

Source: Authors’ computations on simulation results (2008–2050).

{kind=link}

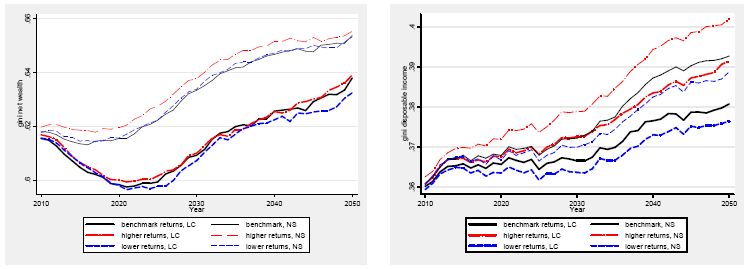

Evolution in the Gini of net worth (left) and disposable income (right), 2010–2050.

Source: Authors’ elaboration on simulation results.

{kind=link}

Contributions to wealth Gini variation, LC (left) vs. NS (right) simulation, 2008–2050.

{kind=link}

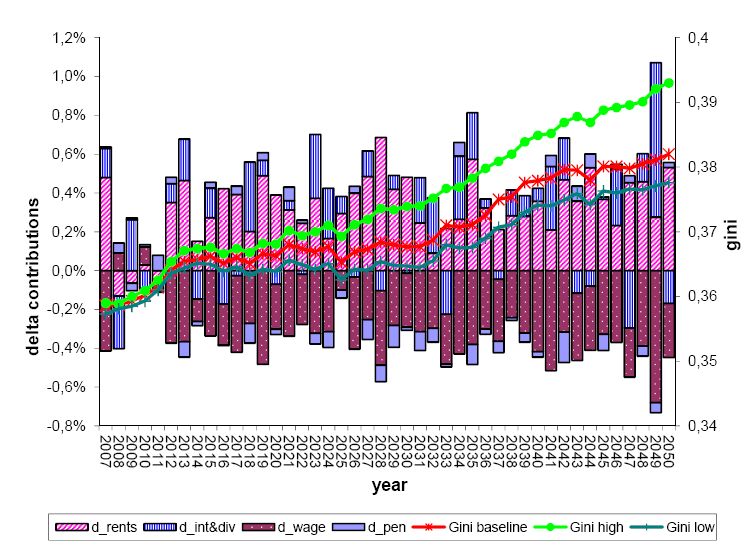

Differential contributions to disposable income Gini variation between high and low returns scenarios, 2007–2050.

Source: Authors’ computations on simulated data.

Tables

Three-stage least-squares regression of planned age of retirement and the expected replacement rate.

| Equation | Obs | Parms | RMSE | R-sq | chi2 | P | |||

|---|---|---|---|---|---|---|---|---|---|

| 1. PRA | 27194 | 21 | 3.435451 | 0.257 | 9408.45 | 0 | |||

| 2. ERR | 27194 | 21 | 0.163388 | 0.149 | 5043.9 | 0 | |||

| Planned Age of Retirement | Expected Replacement Rate | ||||||||

| B | SE | B | Se | ||||||

| year_contrib | −0.5187 *** | 0.0138 | PRA | 0.0026 ** | 0.0010 | ||||

| year_contrib² | −0.0093 *** | 0.0003 | year_contrib | 0.0064 *** | 0.0009 | ||||

| age*contrib. | 0.0148 *** | 0.0003 | age*contrib | 0.0000 | 0.0000 | ||||

| female | −2.0137 *** | 0.0523 | NDC | −0.0292 | 0.0180 | ||||

| NDC | 0.1496 | 0.3824 | single | −0.0024 | 0.0050 | ||||

| Education (omit.lower secondary) | |||||||||

| upper_secondary | 0.2877 *** | 0.0557 | upper secondary | 0.0130 *** | 0.0026 | ||||

| degree_or_more | 0.8929 *** | 0.0842 | degree or more | 0.0094 * | 0.0040 | ||||

| self_employed | 1.2709 *** | 0.0646 | self employed | −0.1168 *** | 0.0033 | ||||

| public | −0.2373 *** | 0.0632 | public | 0.0457 *** | 0.0030 | ||||

| home_owner | −0.1369 * | 0.0564 | partime | −0.0363 *** | 0.0047 | ||||

| South | 0.6384 *** | 0.0580 | Centre | 0.0321 *** | 0.0030 | ||||

| single | 0.3774 *** | 0.1072 | South | 0.0427 *** | 0.0030 | ||||

| tau2002 | 0.0625 | 0.0751 | tau2002 | −0.0298 *** | 0.0035 | ||||

| tau2004 | 0.2979 *** | 0.0774 | tau2004 | −0.0453 *** | 0.0036 | ||||

| tau2006 | 0.0922 | 0.0805 | tau2006 | −0.0739 *** | 0.0037 | ||||

| tau2008 | 0.8402 *** | 0.0978 | tau2008 | −0.0793 *** | 0.0047 | ||||

| Cohort effect (omit. Cohorts <1953) | |||||||||

| coor_53 | 1.1369 *** | 0.1010 | coor_53 | 0.0122 ** | 0.0046 | ||||

| coor_58 | 2.0562 *** | 0.1234 | coor_58 | 0.0165 ** | 0.0056 | ||||

| coor_63 | 2.5093 *** | 0.1462 | coor_63 | 0.0257 *** | 0.0065 | ||||

| coor_68 | 2.5112 *** | 0.1672 | coor_68 | 0.0393 *** | 0.0071 | ||||

| coor-73 | 2.3387 *** | 0.1844 | coor-73 | 0.0660 *** | 0.0075 | ||||

| coor_78 | 2.0769 *** | 0.2041 | coor_78 | 0.0688 *** | 0.0081 | ||||

| intercept | 61.3483 *** | 0.1937 | intercept | 0.4269 *** | 0.0635 | ||||

| Endogenous variables: PRA, ERR | |||||||||

-

*

p<.05.

-

**

p<.01.

-

***

p<.001.

-

Source: Authors’ computations on SHIW 2000–2008.

Dynamic panel-data estimation of the consumption rule, two-step system GMM 16.

| ln{C/HR} | B | Se |

|---|---|---|

| Lag.ln{C/HR} | 0.0821 *** | 0.0209 |

| In_af_en | 0.0114 *** | 0.0024 |

| In_ar_h | −0.0171 *** | 0.0014 |

| In_ar_h*n_houses | 0.0040 *** | 0.0006 |

| In_pf | 0.0092 *** | 0.0012 |

| quintile 2_income | −0.1347 *** | 0.0181 |

| quintile 3_income | −0.1832 *** | 0.0206 |

| quintile 4_income | −0.2559 *** | 0.0232 |

| quintile 5_income | −0.3105 *** | 0.0272 |

| hh_age | −0.2152 *** | 0.0491 |

| hh_age² | 0.0066 *** | 0.0013 |

| hh_age³ | −0.0001 *** | 0.0000 |

| hh_age4 | 0.0000 *** | 0.0000 |

| hh_age_self_emp | −0.0026 *** | 0.0004 |

| hh_age_upper_secondary | −0.0009 *** | 0.0002 |

| hh_age_degree_or_more | −0.0032 *** | 0.0004 |

| h_res_life | −0.0143 *** | 0.0027 |

| hh_retired | −0.1282 *** | 0.0213 |

| earners_ratio | −0.2058 *** | 0.0326 |

| n_child_in the family | 0.0232 ** | 0.0087 |

| South | −0.0489 *** | 0.0109 |

| Household types (omitt. Nuclear family) | ||

| Single | 0.0108 | 0.0211 |

| nuclear single headed | 0.1754 *** | 0.0356 |

| non_nuclear single headed | 0.4704 *** | 0.0350 |

| non_nuclear | 0.1948 *** | 0.0174 |

| Time dummies (omit.tau2002) | ||

| tau1993 | 0.0148 | 0.0191 |

| tau1995 | 0.0623 ** | 0.0193 |

| tau1998 | −0.0699 *** | 0.0210 |

| tau2000 | −0.4194 *** | 0.0194 |

| tau2004 | −0.0219 | 0.0176 |

| tau2006 | 0.0228 | 0.0186 |

| tau2008 | 0.0018 | 0.0182 |

| intercept | −0.2847 | 0.6923 |

-

N = 23,426, number of groups = 10,284.

-

Arellano-Bond test for AR(1) in first differences: z = −18.00 Pr > z = 0.000.

-

Arellano-Bond test for AR(2) in first differences: z = 0.49 Pr > z = 0.627.

-

Sargan test of overid. restrictions: chi2(7) = 7.60 Prob > chi2 = 0.369.

-

Hansen test of overid. restrictions: chi2(7) = 4.79 Prob > chi2 = 0.685.

-

Difference-in-Hansen tests of exogeneity of instrument subsets:

-

GMM instruments for levels.

-

Hansen test excluding group: chi2(6) = 4.60 Prob > chi2 = 0.596.

-

Difference (null H = exogenous): chi2(1) = 0.20 Prob > chi2 = 0.658.

-

*

p<.05.

-

**

p<.01.

-

***

p<.001.

-

Source: Authors’ computations on SHIW data, Historical Archive, panel component, waves 1991–2008.

Two-step estimation for intergenerational giving with Heckman correction.

| Donor side N=16,871 | |||||

|---|---|---|---|---|---|

| Logit Probability of being Donor | OLS ln{Ratio} | ||||

| B | Se | B | Se | ||

| age | 0.0807 *** | 0.0243 | age | −0.7785 ** | 0.2404 |

| age2 | −0.0007 *** | 0.0002 | age2 | 0.0113 ** | 0.0036 |

| in_work | 0.3522 *** | 0.052 | age3 | −0.0001 ** | 0.000 |

| quintile 3_wealth | 0.4146 *** | 0.0543 | in work | −0.4384 *** | 0.0866 |

| quintile 4_wealth | 0.6046 *** | 0.0531 | retired | −0.2449 ** | 0.0849 |

| quintile 5_wealth | 0.6989 *** | 0.0531 | unemp | −0.4619 ** | 0.1649 |

| child_unemp | 0.2835 *** | 0.0625 | ch_unemp | 0.3006 *** | 0.0817 |

| wed_or_birth | 3.2668 *** | 0.1205 | quintile 3_wealth | −0.5422 *** | 0.0752 |

| upper_secondary | 0.5074 *** | 0.0463 | quintile 4_wealth | −0.8931 *** | 0.0736 |

| degree_or_more | 0.742 *** | 0.0502 | quintile 5_wealth | −1.4278 *** | 0.0733 |

| Italy | −0.2737 *** | 0.0747 | Italy | 0.7029 *** | 0.0951 |

| _intercept | −4.4368 *** | 0.8158 | mills_ratio | 0.2653 *** | 0.0414 |

| _intercept | 15.5409 ** | 5.3305 | |||

-

T

-

*

p<.05.

-

**

p<.01.

-

***

p<.001.

-

Source: Authors’ computations on SHARE data, wave 2004.

Two-step estimation for intergenerational receiving without Heckman correction.

| Recipient side | |||||

|---|---|---|---|---|---|

| N=29,652 Logit Probability of being Recipient | N= 1,872 OLS ln{Amount} | ||||

| B | t | B | Se | ||

| In(af parents) | 0.169 *** | 0.061 | In(af parents) | 0.0892 *** | 0.0079 |

| age | −0.0883 *** | 0.052 | age | 0.0253 * | 0.0147 |

| age² | 0.0007 *** | 0.0543 | age² | −0.0004 * | 0.0002 |

| married | 0.3004 ** | 0.0531 | grandchildren | −0.1051 * | 0.0567 |

| single | 0.6497 *** | 0.0531 | married | 0.1911 *** | 0.0494 |

| divorced | 0.6462 *** | 0.0625 | Italy | 0.2481 ** | 0.0944 |

| in work | −0.2689 *** | 0.1205 | _intercept | 7.028 *** | 0.2699 |

| degree | 0.3421 *** | 0.0463 | |||

| grandchildren | 0.2863 *** | 0.0502 | |||

| Italy | 0.1984 ** | 0.0747 | |||

| _intercept | −1.3815 *** | 0.8158 | |||

-

T

-

*

p<.05.

-

**

p<.01.

-

***

p<.001.

-

Source: Authors’ computations on SHARE data, wave 2004.

Cumulated contributions to wealth Gini variation, LC vs. NS simulation, 2008–2050 (in percent).

| W0 | Capgains | S | ig_tr | ESA | d.gini | |

|---|---|---|---|---|---|---|

| 1.LC approach | 0.146 | −3.918 | −0.511 | 6.757 | −1.958 | 0.516 |

| 2.NS approach | 0.128 | −4.522 | 6.754 | 2.979 | −1.705 | 3.634 |

| (1)– (2) | −0.018 | −0.604 | 7.264 | −3.778 | 0.253 | 3.118 |

-

Source: Authors’ computations on simulated data.

Cumulated contributions to disposable income Gini variation, LC approach, different returns scenarios, 2008–2050 (in percent).

| After_tax pensions | After-tax earnings | Rents on real estate net of liabilities | Interests on financial wealth | d.gini | avg r-g | |

|---|---|---|---|---|---|---|

| 2.low returns | 5.55 | −1.42 | 2.50 | 3.51 | 10.13 | 0.13 |

| 1.Benchmark | 5.28 | −6.69 | 7.57 | 4.92 | 11.08 | 0.61 |

| 3.High returns | 4.79 | −14.70 | 16.89 | 6.89 | 13.88 | 1.28 |

| (3)-(2) | −0.76 | −13.28 | 14.40 | 3.39 | 3.75 | 1.15 |

-

Source: Authors’ computations on simulated data.

Cumulated variation in incomes shares (in percent).

| Sources | 2008 | 2050 | 2050–2008 | 2008 | 2050 | 2050–2008 | 2008 | 2050 | (2050)-(2008) |

|---|---|---|---|---|---|---|---|---|---|

| After-tax earnings | 51.0 | 43.8 | −7.2 | 51.4 | 46.2 | −5.2 | 50.7 | 40.0 | −10.7 |

| After-tax pensions | 29.7 | 29.7 | 29.9 | 31.3 | 1.5 | 29.5 | 27.2 | −2.3 | |

| Rents on real estate net of negative interests | 14.6 | 18.3 | 3.7 | 14.1 | 15.1 | 1.1 | 15.2 | 23.7 | 8.6 |

| Interests on financial wealth | 4.7 | 8.2 | 3.4 | 4.7 | 7.4 | 2.7 | 4.7 | 9.1 | 4.4 |

-

Source: Authors’ computations on simulated data.

Table A1 Exogenous parameters (per year).

| Low returns scenario | Benchmark returns scenario | High returns scenario |

|---|---|---|

| Productivity | Productivity | Productivity |

| Same as benchmark | G (average earnings growth) | Same as benchmark |

| “ | 0.88% (2008–2009) | “ |

| “ | 1.00% (2010–2013) | “ |

| “ | 1.20% (2014–2019) | “ |

| “ | 1.90% (2020–2029) | “ |

| “ | 2.00% (2030–2050) | “ |

| Capital gains | Capital gains | Capital gains |

| rh ~N µ=0.75%; sd=8% | rh ~N µ= 1.5%; sd= 8% | rh ~N µ=2.5%; sd=8% |

| rf ~N µ=1.5%; sd=18%; | rf ~N µ=3%; sd=18%; | rf ~N µ=5%; sd=18%; |

| kurt = 2.4% | kurt=2.4% | kurt=2.4% |

| resa=0.9% | resa=0.9% | resa=0.9% |

| Interests and rents | Interests and rents | Interests and rents |

| Same as benchmark | rm ~N µ=3%; sd= 0.5% | Same as benchmark |

| “ | home equity annual rent: 3.5% | “ |

| “ | real interest rate on non-risky AF: 1% | “ |

| “ | real interest rate on risky AF: 3% | “ |