Policy transparency in the public sector: The case of social benefits in Tanzania

- Southern African Social Policy Research Insights, United Kingdom

- University of Dar es Salaam, Tanzania

- Southern African Social Policy Research Institute NPC, South Africa

- Article

- Figures and data

- Jump to

Figures

{kind=link}

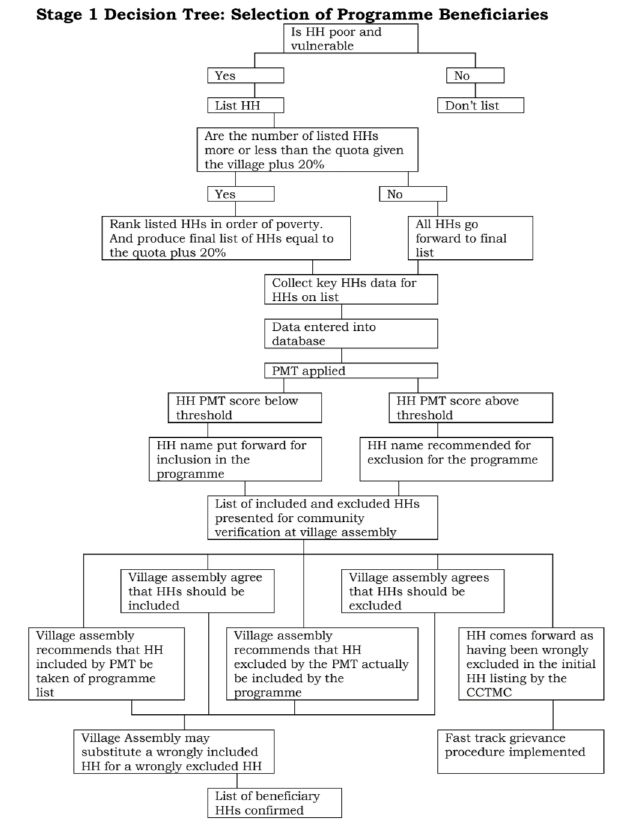

PSSN eligibility decision tree.

Tables

Basic cash transfer and variable cash transfer amounts payable.

| Transfer type | Transfer name | ‘Co-responsibility’ | Benefit (TZS) | Monthly cap (TZS) | Annual max (TZS) |

|---|---|---|---|---|---|

| Fixed | Basic Transfer | Extreme poverty | 10,000 | 10,000 | 120,000 |

| Fixed | Household child benefit | HH with children under 18 | 4.000 | 4,000 | 48,000 |

| Variable | Infant benefit | Infants 0–5 health compliance | 4,000 | 4,000 | 48,000 |

| Variable | Individual primary benefit | Child in primary education compliance | 2,000 | 8,000 | 96,000 |

| Variable | Individual lower secondary benefit | Child in lower secondary education compliance | 4,000 | 12,000a | 144,000 |

| Variable | Individual upper secondary benefit | Child in upper secondary education compliance | 6,000 |

-

Source: World Bank et al. (2016, p. 16).

-

a

The two bottom rows in combination may not total more than TZS 12,000 per month.

Basic cash transfer and variable cash transfer amounts payable.

| System (2017) Scenario | Description | Net cost (compared to baseline) TZS Million | Poverty (Basic Needs) % | Poverty (Food Poverty) % | Inequality (Gini) |

|---|---|---|---|---|---|

| 2017 | Baseline (includes PSSN) | 0 | 29.1 | 6.4 | 0.390 |

| A | No PSSN | −194,198 | 29.1 | 10.9 | 0.397 |

| B1 u5s | Universal Child Benefit for u5s (TZS15,000 pcmb), no PSSN. | 1,135,303 | 24.5 | 7.2 | 0.382 |

| B2 u4s | Universal Child Benefit for u4s (TZS15,000 pcm), no PSSN. | 814,023 | 25.6 | 8.0 | 0.385 |

| C | Universal Old Age Benefit for those aged 70+ (TZS15,000 pcm), no PSSN. | 22,168 | 28.6 | 10.3 | 0.395 |

| D | Universal Disability Benefit (TZS15,000 pcm), no PSSN. | 18,290 | 28.5 | 10.5 | 0.395 |

| E1 u4s | All three Universal Benefits (TZS15,000 pcm), no PSSN. | 1,242,878 | 24.5 | 7.2 | 0.382 |

| E2 u4s | All three Universal Benefits (TZS15,000 pcm), no PSSN. PIT rates increased. | −96,431 | 25.2 | 7.7 | 0.375 |

| F | Basic Income Grant (TZS 10,000 pcm), no PSSN. | 4,878,217 | 12.5 | 1.6 | 0.349 |

-

Source: Own analysis using TAZMOD V1.7.

-

Notes: In scenario E2, all tax thresholds are the same as for the Baseline, as are the rules for turnover tax and the first band of Personal Income Tax (PIT). The tax rates for other bands were increased as follows: Band 2 raised from 9 per cent to 12 per cent; Band 3 raised from 20 per cent to 25 per cent; Band 4 raised from 25 per cent to 30 per cent; and Band 5 (the top band) raised from 30 per cent to 37 per cent. This scenario is included as an example only. Further work is underway on the income data in the dataset, which will improve the robustness of estimates that use employment income data.

-

b

pcm (per calendar month)